Healthcare Spending Accounts (often referred to as HCSA or HSA) are essentially a bucket of money that can be spent on anything on the CRA eligible medical expenses list. HCSA’s can be used to supplement or replace parts of a traditional benefits plan. For example, a company may choose to offer the basic restorative and Periodontic-Endodontic levels of dental coverage, but instead of the higher, more expensive levels of dental they could offer a $1000 HCSA to help offset the price of expensive dental work. Note that in this scenario, the HCSA can be used to pay for anything on the eligible expenses list, not just dental work.

HCSA Components:

There are many components of the HCSA benefit. The following is not intended to be an exhaustive list, rather these are the most common components:

.

HCSA amount:

The amount of money available under the Healthcare Spending Account. Note that this amount can differ by class.

.

Benefit period:

Whether or not the HCSA period is based on a benefit year (ie the 12 months from when the group benefits plan renews) or a calendar year basis (1st Jan – 31st Dec).

.

Allocation period:

How the HCSA amount is made available. This could be annually (ie the full amount right away) bi-annually (half now, the other half in six months) or even quarterly. The allocation period can help to control risk in classes with high turnover, avoiding the situation where employees with short tenure max out their HCSA allowance before they leave.

.

Pro-rate new employees:

Determine whether employees joining partway through the year get the full HCSA amount or a pro-rated amount (for example an employee joining six months into the benefit period would receive 50% of the HCSA amount for the remainder of the benefit period)

.

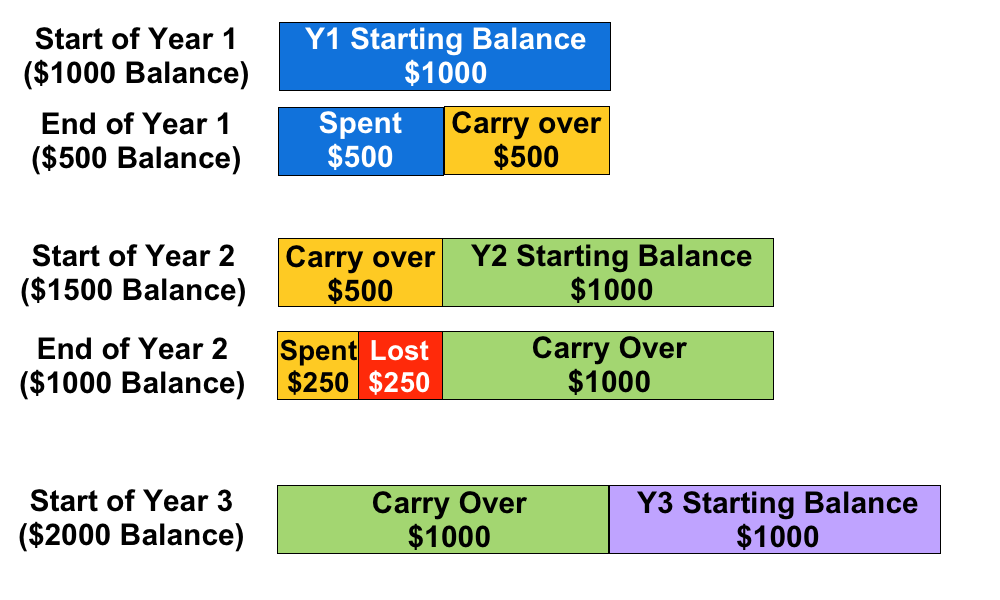

Balance Carry Forwards:

This determines wether or not employees can carry their remaining HCSA balance from one year to the next. This is typically restricted to one year only. The carried over balance is used to cover claims first, before the new balance is used.

For example, if an employee has a $1000 annual HCSA allocation and they only use $500, the next year they will have $1500 available in their HCSA. However, if they only use $250 in the second year, they can only transfer $1000 to Year 3, even though $1250 is remaining in their HCSA. Note that the remaining $250 is forfeit, it cannot be paid out to the employee.

.

An example showing how Balance Carry Forwards works

.

Benefits of a HCSA

- They are flexible: The money can be spent on anything that is deemed an eligible expense. This avoids a situation where employees maxes out their coverage in one area of the plan, but still has a lot of unused coverage in other areas (this is common with items such as paramedical practitioners)

- They help prevent employees being out of pocket: Deductibles, dispensing fees and other out of pocket expenses from the regular benefits plan can be claimed under a HCSA.

- Tax advantages: HCSA claims are a tax deductible business expense, and the benefits are received tax-free, provided the HCSA is 100% employer paid. Unused HCSA amounts cannot be paid out at year-end as cash to the employees, any unused amounts that are not eligible to be carried forwards are forfeited by the employee.

- Employees can save up for larger expenses: If an employee has expensive treatment that can be scheduled, such as laser eye surgery, they can take advantage of Barry Carry Forwards to maximize how much they can claim using their HCSA.

.

Potential challenges

- There is no way to limit what the HCSA is used for: Provided the claim is deemed eligible under the guidelines there are no other restrictions placed on what can be claimed under the HCSA. The guidelines may be broader than a traditional benefits plan.

- HCSA’s are an ASO benefit: This means the employer is entirely responsible for covering every dollar spent under an ASO, along with any applicable administration fees. Combined with the point above, make sure your plan sponsor is able to cover the costs if a large % of employees use most of all of their available HCSA amounts (taking into account the additional risk of Balance Carry Forwards). While this scenario is unlikely, making sure the plan sponsor is prepared for it will help to avoid any unpleasant surprises.

- May create cash flow fluctuations: It is important to check the ASO funding model being used by the HCSA benefit. ‘Pay-as-you-go’ is a popular model, meaning the plan sponsor is responsible for the HCSA claims almost immediately. This can create large fluctuations in benefit costs month to month.

Deprecated: Function get_magic_quotes_gpc() is deprecated in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/formatting.php on line 4387

Deprecated: Function get_magic_quotes_gpc() is deprecated in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/formatting.php on line 4387

Deprecated: Function get_magic_quotes_gpc() is deprecated in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/formatting.php on line 4387