Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Unfortunately Plan Administrators are rarely experts in group insurance and are likely responsible for more than just their PA duties. Plan Administrators have access to large amounts of sensitive employee data, such as dates of birth, dependant details and salaries. It is therefore important to choose the correct person for this role.

Here are a few of the items that a Plan Administrator is responsible for on a regular basis:

- Updating salary information: Salaries often change annually, but can also change at any point in the year due to promotions or pay raises. Several group benefits such as Life, Short Term Disability and Long Term Disability have premiums based on an employee’s salary. Any claims for these benefits will use the salary information currently on record for that employee (as that is what their premiums have been based on). Not keeping salaries up to date can have serious consequences, for example an employee’s disability benefit could be lower than anticipated because it is based on their salary from several years ago. Because the premiums for these benefits are often salary based, updating a certificates salary details in the admin system will likely increase the premiums they are paying.

. - Updating employee’s key information: Employee details change over time and can have a material impact on their employee benefits. Perhaps they recently got married or had a child, which means new dependant information to capture and potentially a change in their family status. Job changes can impact an employee’s salary, but it can also impact which benefits class they are in (for example moving from the regular employees class into the management class). Switching from part time to full time, or vice versa, could impact their eligibility for group benefits. All of these things need to be tracked in the admin system by the PA.

. - Adding new employees: Timely enrolment of new employees is important to ensure they receive their appropriate coverage without penalty. Insurers can impose restrictions on coverage or require additional medical evidence for employees that are considered late enrolee’s in the plan.

. - Cancelling employees: Just as important as adding new customers is ensuring that employees are cancelled as soon as they are no longer eligible. This will help to control the group’s overall claims experience. Note that there are several cancellation circumstances that will automatically be handled by the insurance company, for example when employees reach the termination age they will automatically be cancelled.

. - Billing: Plan Administrators are often the ones tasked with handling the monthly invoices for group insurance, ensuring that payments are kept up to date. This is important to ensure that claims are paid promptly.

. - Record keeper: Once a group plan is initially setup it is common for the Plan Administrator to become the key record keeper. This means it will be their responsibility to keep paperwork such as enrolment forms for new employees, rather than sending these in to the insurance company.

. - Supporting Employees: Plan Administrators act as a key resource for employees when dealing with group insurance enquiries. They are often the first port of call for employees questions regarding plan coverage. The expectation is not that PA’s are intimately familiar with the ins and outs of the groups benefit plan (although it certainly helps) but they often provide resources such as replacement benefit booklets, claim forms and important announcements.

. - Pulling together documents: This can start in the marketing phase when the PA will need to provide up to date employee data to the Insurance Advisor to accurately market the group. If the group chooses to switch insurance carriers it often falls to the PA to help gather all the required documentation, such as updated enrolment forms for all employees. The PA may also be involved in distributing the new documents such as new enrolment cards, benefit booklets and marketing materials.

These are just some of the important tasks that PA’s are involved in. Most insurers will provide a handbook or guidance to help PA’s understand their duties and teach them how to use the administration system.

]]>Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

To counteract this, insurance carriers create a buffer of premiums which are to be used to cover claims in the event a group cancels coverage. This buffer is referred to as the IBNR charge and is usually expressed as a % of premiums or as a % of paid claims. This premium is reserved at the end of the first renewal and is held to cover IBNR claims. Therefore this amount is not included in the experience rating renewal calculations. In subsequent renewals the IBNR is recalculated and the previous IBNR is released, which in effect means the customer is only paying for the difference. In this way the IBNR premium being held is always reflecting the most recent experience.

IBNR charges differ between insurance carriers and products and should be reviewed as part of an overall marketing check. Higher IBNR %’s tie up more premiums, which will increase renewal rates. With the advent of more efficient methods for submitting a claim, such as online claims portals, drug cards and smart phone apps, IBNR charges have slowly been reducing as the delay between incurring a claim and reporting it is reducing.

]]>Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Some of the topics that are often covered by EAP’s are:

- Workplace stress

- Substance abuse or smoking cessation

- Disability support

- Grievance counselling

- Relationship issues

- Financial advice

- Legal advice

- Advice for managers on employee situations

Everything discussed with the EAP provider is strictly confidential and is free for the employees and their immediate family to use. The separation of the EAP provider and the employer is a key component of the benefit, enabling employees to talk openly about issues that they may not be comfortable discussing with their employer for fear or reprisals.

The focus of an EAP program is on employee wellness and in being proactive, resolving problems before they impact work performance. The nominal cost is potentially offset by a reduction in absenteeism and turnover, faster recovery and less burden for managers and/or HR. The key is in making employees aware of the EAP program and all that it offers through regular employee communications and information sessions. Under utilization of the EAP benefit is usually due to a lack of awareness of the services available.

.

How does an EAP work?

The initial point of contact with the EAP provider is via a phone call using the number provided. The employee or a member of their immediate family calls this number within the hours of operation (typically 24/7) and speaks to a phone agent that helps them determine the nature of their problem. The agent will either then proceed with the call (if it is within their area of expertise) or refer the caller to an appropriate resource that is suitably trained to handle the issue. A call back time or face to face meeting may be scheduled if no suitable resource is currently available.

.

Options

There are limited options to choose from for most EAP benefits. If there are options they typically centre around the level of EAP services provided, for example whether face to face EAP consultations are available. There may also be choices around the different categories the EAP covers, with topics such as legal advice or financial advice constituting optional extras.

.

Rates

EAP is usually priced on a flat per employee basis. The rate may be bundled with other products (such as EHB or LTD) or sold separately.

]]>Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

It is important to stress that Out of Country is not the same as trip insurance. It only covers medical emergencies and will not pay for cancelled flights, hotel stays as a result of delays or lost luggage. The definition of ‘medical emergency’ varies from carrier to carrier, but it typically means unexpected illnesses or accidental injuries. There may be pre-existing condition exclusions. It is important to review the conditions of your out of country coverage before heading overseas as resolving issues while someone is out of the country can be extremely challenging.

Out of Country components:

Unlike other group benefits, there are relatively few choices regarding Out of Country, with each carrier offering a limited selection of options. However, there are components that should be compared between each carriers OoC offering as these variables can have a significant effect on the coverage available:

.

Number of days covered:

There may be a choice regarding the number of days the out of country benefit covers, but even a standard offering will cover the vast majority of trips. Between 60 and 120 days is the usual amount of days covered. Note that these are typically consecutive days (not annual limits) but there may be rules around what constitutes a continuation of the same journey. For example, returning to your home province for 24 hours but then leaving again may be considered a continuation of the previous trip.

Note that both business and personal travel is covered, and if you have family OoC coverage your eligible dependants are likely also covered under your OoC benefit.

Typically the only employees that run the risk of exceeding the number of days trip limit is business owners that are snow birds (i.e. living overseas for extended periods during the Winter). These employees should confirm that their OoC coverage will cover the duration of their time overseas or purchase additional insurance to fill any gaps in coverage.

.

Students studying overseas:

Extended OoC coverage may be available for students that are studying overseas, but these are typically considered on a case by case basis. Approval should be confirmed with the groups insurance carrier before the student leaves the country. Restrictions often apply, for example coverage may only apply while the student is studying and may not cover any travel they do before or after their courses. There may also be restrictions around which educational institutions and/or countries are covered. It is worth stressing again that the Out of Country benefit only covers medical emergencies.

.

Lifetime Maximum:

Out of country typically operates on a lifetime maximum basis. These maximums can be extremely high (in the millions of dollars) or sometimes even unlimited. Note that there may be other restrictions or limitations regarding what is and isn’t covered, and for how much. It is worth comparing the specifics of each carriers offerings to understand which would provide the most comprehensive coverage.

.

Termination Age:

The age at which employees are no longer covered by the OoC benefit. 75 is the standard OoC term age, but some carriers may offer a higher termination age or a choice of OoC termination ages, with higher OoC rates for older employees.

Note that as with other benefits the Termination Age is applied to the employee. Dependant spouses that exceed the termination age remain covered as long as the employee is under the termination age. This can be particularly important for OoC coverage.

.

Travel Assistance:

The Out of Country benefit often includes a travel assistance portion, which assists employees that are injured or sick while overseas. This assistance can include everything from locating appropriate care facilities nearby, pre-paying medical bills or helping to rearrange transport back to Canada.

It is highly recommended that employees contact the travel assistance provider as soon as possible once a claim incidence has occurred, to help ensure that the claims process is a smooth one for all parties. The number is usually found on the employees benefit card.

.

Coinsurance & Deductible:

As Out of Country coverage is intended to cover emergencies only (ie not a planned spend) they usually have 100% coinsurance, meaning the claimant is not expected to cover any % of the overall costs. For the same reason OoC usually has a $0 deductible.

.

Rates:

Out of Country rates are most commonly based on a flat amount, with certificates with single coverage paying around half as much as those with family coverage. OoC is not an experience rated benefit, it is a pooled benefit. However unlike other pooled benefits OoC is pooled from first dollar, meaning that all claim amounts are pooled and none of the cost is passed on to the policyholder.

.

.

Key Provisions:

- Pre-existing condition/Stability clause: Out of Country is intended to cover unexpected medical emergencies. For this reason there is typically pre-existing conditions or stability clauses in the OoC benefit. These can limit or prohibit OoC claims related to a known medical condition. For example, if an employee had a heart attack, and 2 weeks later went overseas on holiday and had another heart attack, this is unlikely to be covered by the OoC benefit due to this clause. This does not mean that this employee could not claim for a different medical emergency, nor does it mean they can never claim for heart related conditions again – the stability clause will outline how long an employee must be symptom and treatment free before their condition is considered ‘stable’.One common ‘condition’ caught up in the pre-existing clauses is pregnancy. There are often guidelines around at what point in a pregnancy Out of Country would no longer cover the birth of the child. This is a particularly important provision to understand as the cost of delivering and caring for a premature child while overseas can run in to hundreds of thousands of dollars.

- High risk activities: Another common exclusion is activities deemed to be high risk. A full list of these will be included in the OoC contract, but common exclusions include heli-skiing, motor sport racing or competitive sports that you are paid to compete in.

Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Paramed components:

There are many components of Paramed coverage. The following is not intended to be an exhaustive list, rather these are the most common components:

.

Paramed practitioners:

A choice is offered as to which paramed practitioners will be covered by the plan. There are a wide variety of paramed practitioners to choose from, although it is not as simple as just selecting the desired practitioners. Often there are additional requirements, for example practitioners may be required to be licensed, certified or registered.

Typical practitioners to choose from include:

- Acupuncturist

- Audiologist

- Chiropractor

- Chiropodist

- Dietician

- Naturopath

- Occupational Therapist

- Osteopath

- Physiotherapist

- Podiatrist

- Psychologist

- Registered Massage Therapist

- Social Worker

- Speech Therapist

.

Coinsurance:

How much of the cost of the practitioner is covered by the employer. Lower coinsurances (for example 50%) create more out of pocket expenses for employees, but may also help to reduce utilization and/or fraudulent claims.

.

Maximum:

There are several different ways the paramed maximum can be calculated. The calculation you choose will depend on the level of cost containment desired. Here are some of the available options:

- Per Certificate, per practitioner: This option combines the claims experience of everyone under one certificate (employee + spouse + dependants) on a per practitioner basis. For example, if there was a $300 maximum in this scenario, if one family member claimed $300 of physio then no other members of that certificate could claim physio until the next benefit period. They could however claim for a different practitioner, for example a speech therapist.

- Per Insured, per practitioner: This option provides a separate maximum for each member under one certificate (employee + spouse + dependants) on a per practitioner basis. For example, if there was a $300 maximum in this scenario, each member of the family could claim up to $300 of physio per benefit period. This option creates the greatest opportunity for risk.

- Per Certificate, All practitioners combined: This option combines the claims experience of everyone under one certificate (employee + spouse + dependants) and across all practitioners. It therefore is the option with the lowest risk (although this may not be true if a higher overall maximum is used). For example, if there was a $500 maximum in this scenario, once the combined claims of all family members reaches $500, no additional parameds can be claimed until the next benefit period.

- Per Insured, All practitioners combined: This option combines the claims experience of all practitioners for each individual member of the certificate. For example, if there was a $500 maximum in this scenario, one family member reaching the $500 maximum across all practitioners has no bearing on the other family members ability to make paramed claims.

- Maximum per visit, per insured: This option can often be used in conjunction with one of the maximums selected above. It further restricts paramed coverage by capping the amount that can be claimed per visit. For example, if this maximum was set to $100, then an insured is only reimbursed up to $100 per visit, even if the amount of the claim is higher. There is often an option to differ the maximum amount by practitioner.

.

Referral required:

If this option is selected then insureds need to get a referral from their physician before they can make a paramed claim. This option is most often applied to massages. There is some debate as to how effective a deterrent this is.

]]>Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

The Critical Illness benefit is designed to reduce the financial strain for employees, allowing them to focus on their recovery.

Critical Illness Components:

There are many components of the Critical Illness benefit. The following is not intended to be an exhaustive list, rather these are the most common components:

.

Covered Conditions:

The number of conditions that are covered by the Group CI benefit. The list of covered CI conditions continues to increase, with carriers regularly adding more conditions. Note that 85%+ of all CI claims will fall under a very small subset of CI conditions, stroke, heart attack, cancer and coronary artery bypass surgery. Plans covering more conditions may appear to be offering greater protection, but these may come at the cost of more stringent pre-ex requirements or lower NEM‘s.

Note that some Group CI plans will cover dependants, either spouse, children or both. It is not uncommon for the list of conditions covered to differ for children.

.

Lump Sum Amount:

The $ amount paid to the employee when they are diagnosed with a covered condition and all the other criteria are met. The lump sum payment is tax free and there are no restrictions on how it is used. It does not have to be spent on medical expenses, for example the employee could choose to spend it on a family vacation or use it to pay off existing debts.

..

Termination Age:

The age at which the Critical Illness benefits cease to be paid. 70 is a commonly used termination age for CI, although higher termination ages may be available depending on the carrier.

.

Reduction Schedule:

Similar to the Group Life benefit, Group CI often has a reduction schedule, meaning that the amount of coverage provided decreases once an employee reaches a certain age. For example, the benefit may drop by 50% once the employee reaches age 65, meaning if the lump sum benefit is $50k, an employee over 65 that has an approved CI claim would receive $25k.

.

Pre-existing Condition Guidelines:

Group CI pre-existing condition (pre-ex) guidelines are typically expressed in two numbers, separated by a /, for example 12/12. A 12/12 pre-ex means that any CI claim within 12 months of the effective date would not be paid if the employee had sought medical attention or had symptoms related to said condition at any point during the 12 months prior to the effective date. Pre-ex exists to prevent employees from seeking Group CI coverage when they know or suspect that they may have a critical illness. Longer pre-ex periods provide greater protection from anti-selection and will help lower the cost of the Group CI benefit.

.

Partial Payment:

Some Critical Illness plans offer a reduced lump sum payout if an employee is diagnosed with a condition on the partial benefits list. These often include early diagnosis of cancer. Claiming a partial benefit does not typically effect your ability to make a full CI claim down the road if your are later diagnosed with a condition on the lump sum payment list.

.

Multiple Payments:

Some Critical Illness plans will pay for more than one CI claim. Do be aware though that restrictions apply. You can’t claim the same condition twice, for example if you had a heart attack and later had a second heart attack (although see below regarding cancer). In addition to this, conditions are usually classified into categories or groups, and it is not possible to claim multiple conditions from the same category.

An example of condition categories

For example, if an employee was diagnosed with Condition A from the chart above and received a full payout, and was later diagnosed with Condition B, they would not be eligible to receive the second payout as both conditions are in the same category. However, if they were diagnosed with Condition Z, that is in a different category and the second claim would be eligible.

Note that the number of categories and which conditions are in them can differ between insurance carriers.

.

Cancer Recurrence:

Some Critical Illness plans will pay for more than one cancer CI claim. This may be treated differently from the regular multiple payments detailed above. There are usually clear guidelines as to how and when multiple cancer claims would be eligible, for example, after 5 years treatment free.

.

Benefits of Critical Illness

- You’re helping employees when they need it most: Being diagnosed with a serious condition is stressful enough, without having the added burden of day to day finances. Knowing that they have Group CI coverage can help provide peace of mind for all employees.

. - The benefit is extremely flexible: The employee can choose how best to spend the lump sum payment, based on their individual circumstances, making Group CI a very flexible way to provide support.

.

Potential challenges

- Understand the restrictions: Different carriers will cover a variety of conditions for CI, some up to 40 different conditions. Note that the number of conditions is not as important as the restrictions around those conditions. More important than the number of conditions are the restrictions placed on CI coverage, for example:

- Pre-ex requirements: See above. Longer pre-ex periods can make it harder to make a claim.

- Survival period: How long the employee must survive before the lump sum payment is paid out.

- Non-evidence maximums: How much coverage is available without medical evidence. More details on NEM’s can be found here.

.

- Moving groups with Critical Illness: Group CI benefits have a lot of behind the scenes rules and guidelines that can vary significantly from carrier to carrier. Be especially aware when moving a group with CI from one carrier to another, as employees that may have previously been eligible for coverage may no longer be covered due to the new carriers restrictions, condition categories etc. Be sure to check what (if anything) will be covered by grandfathering. For example, what is the impact on an employee halfway through their pre-ex period when the group transfers?

Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

HCSA Components:

There are many components of the HCSA benefit. The following is not intended to be an exhaustive list, rather these are the most common components:

.

HCSA amount:

The amount of money available under the Healthcare Spending Account. Note that this amount can differ by class.

.

Benefit period:

Whether or not the HCSA period is based on a benefit year (ie the 12 months from when the group benefits plan renews) or a calendar year basis (1st Jan – 31st Dec).

.

Allocation period:

How the HCSA amount is made available. This could be annually (ie the full amount right away) bi-annually (half now, the other half in six months) or even quarterly. The allocation period can help to control risk in classes with high turnover, avoiding the situation where employees with short tenure max out their HCSA allowance before they leave.

.

Pro-rate new employees:

Determine whether employees joining partway through the year get the full HCSA amount or a pro-rated amount (for example an employee joining six months into the benefit period would receive 50% of the HCSA amount for the remainder of the benefit period)

.

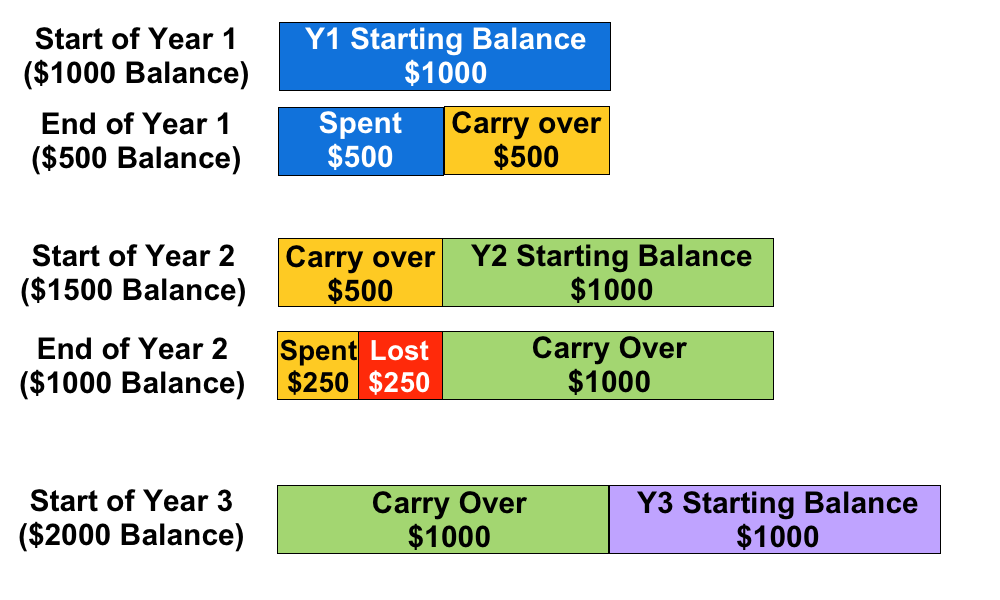

Balance Carry Forwards:

This determines wether or not employees can carry their remaining HCSA balance from one year to the next. This is typically restricted to one year only. The carried over balance is used to cover claims first, before the new balance is used.

For example, if an employee has a $1000 annual HCSA allocation and they only use $500, the next year they will have $1500 available in their HCSA. However, if they only use $250 in the second year, they can only transfer $1000 to Year 3, even though $1250 is remaining in their HCSA. Note that the remaining $250 is forfeit, it cannot be paid out to the employee.

.

An example showing how Balance Carry Forwards works

.

Benefits of a HCSA

- They are flexible: The money can be spent on anything that is deemed an eligible expense. This avoids a situation where employees maxes out their coverage in one area of the plan, but still has a lot of unused coverage in other areas (this is common with items such as paramedical practitioners)

- They help prevent employees being out of pocket: Deductibles, dispensing fees and other out of pocket expenses from the regular benefits plan can be claimed under a HCSA.

- Tax advantages: HCSA claims are a tax deductible business expense, and the benefits are received tax-free, provided the HCSA is 100% employer paid. Unused HCSA amounts cannot be paid out at year-end as cash to the employees, any unused amounts that are not eligible to be carried forwards are forfeited by the employee.

- Employees can save up for larger expenses: If an employee has expensive treatment that can be scheduled, such as laser eye surgery, they can take advantage of Barry Carry Forwards to maximize how much they can claim using their HCSA.

.

Potential challenges

- There is no way to limit what the HCSA is used for: Provided the claim is deemed eligible under the guidelines there are no other restrictions placed on what can be claimed under the HCSA. The guidelines may be broader than a traditional benefits plan.

- HCSA’s are an ASO benefit: This means the employer is entirely responsible for covering every dollar spent under an ASO, along with any applicable administration fees. Combined with the point above, make sure your plan sponsor is able to cover the costs if a large % of employees use most of all of their available HCSA amounts (taking into account the additional risk of Balance Carry Forwards). While this scenario is unlikely, making sure the plan sponsor is prepared for it will help to avoid any unpleasant surprises.

- May create cash flow fluctuations: It is important to check the ASO funding model being used by the HCSA benefit. ‘Pay-as-you-go’ is a popular model, meaning the plan sponsor is responsible for the HCSA claims almost immediately. This can create large fluctuations in benefit costs month to month.

Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

The dental procedures that are covered vary greatly depending on the levels of Dental covered under the plan.

Dental Levels

Dental is typically split into four levels:

- Basic Restorative: This covers diagnostic and preventative treatments, such as cleanings, scaling of teeth, dental examinations, x-rays, oral hygiene, fillings and tooth extractions.

- Periodontic-Endodontic: Includes periodontic services to treat the bone and gum around the tooth and endodontic services.

- Major Restorative: This covers crowns, dentures, inlays, onlays and bridgework. Other more extensive dental may also be covered, including major dental surgery and root canals.

- Orthodontic: This covers appliances such as braces, wires, spacers and other dental aids used to straighten teeth or correct other problems. Pre-approval is often required before proceeding with Orthodontic work. Orthodontics often has a higher co-insurance and a lifetime maximum (as opposed to an annual maximum). One other choice to be made is whether or not to extend Orthodontic coverage to adults or only to child dependants.

.

Dental components:

There are many components of the Dental benefit. The following is not intended to be an exhaustive list, rather these are the most common components:

.

Funding model:

Due to it’s relatively low risk of extremely high claims and fairly stable experience, Dental is often a strong candidate for the Administrative Services Only (ASO) funding model. ASO means that the client takes on the full risk of claims payment themselves and pays the insurance carrier a small administration fee per claim. This mitigates the risk of the policy owner overpaying for their Dental benefit, for example if Dental claims were lower than anticipated and were considerably less than the Dental premium paid. However it also means the client is fully responsible if Dental claims are higher than anticipated.

.

Scaling Units

Scaling units are a measurement of time spent scaling the teeth to remove plaque. These units are measured in 15 minute increments. When employees go to the dentist for their regularly scheduled cleanings, this is typically when scaling units are used, with multiple scaling units charged per visit (typically 2-3, depending on how long was spent scaling the teeth).

Scaling units often have their own maximum as part of the plan design, for example 12 scaling units per period. It is important for employees to know the scaling units maximum on their plan, and also how many scaling units the dentist is charging per visit, to ensure they aren’t left with an expensive out of pocket charge.

.

Recall period:

This determines the length of time required between regularly scheduled dental visits. The most common recall period is 6 months, but 9 or 12 months are also available. Longer recall periods reduce the cost of the dental benefit.

.

Coinsurance:

Coinsurance defines what % of a dental claim the insurance carrier will pay. Lower coinsurances leave the employees covering more of the cost, which reduces the dental claims experience and lowers the dental rates. Note that unlike deductibles, coinsurance continues to be paid for every dental claim, there is no annual limit on the out of pocket expenses for the employee.

.

Deductible:

This works the same way as other insurance deductibles, it is an annual out of pocket expense that the employee must satisfy before a dental claim is paid. Deductibles are different for single and family certs, for example the single deductible may be $50 and the family deductible may be $100. Deductibles are reset every 12 months.

For groups switching carriers late in the calendar year it is often worth getting a report of which employees have satisfied their deductibles, or if such a report is not available asking the new carrier to waive deductibles for all employees for the remainder of the year. This ensures employees are not being penalized by a change in carriers.

.

Maximum:

The maximum $ amount that will be paid out over a 12 month period. There are separate maximums for each level of dental, with options to combine level 3 dental with levels 1&2 to better control costs. Level 4 dental has a lifetime maximum as opposed to an annual max. There may also be a choice for the maximum to be calculated per certificate (ie employee and all dependants combined) or per insured (each family member gets their own maximum).

.

Waiting Period:

The Dental waiting period determines the length of time a new employee must wait before their dental coverage becomes activate. Longer waiting periods can be used in high turnover classes to help reduce the risk of new employees gaining employment solely to utilize the dental benefit. Note however that longer waiting periods can make things difficult for new employees that had dental coverage at their previous employer and now find themselves without dental coverage for an extended period of time.

.

Termination Age:

The age at which the Dental benefits cease to be paid. 75 is the standard Dental term age, but several carriers will allow Dental coverage up to age 85 or even beyond.

]]>Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Life components:

There are many components of the Group life benefit. The following is not intended to be an exhaustive list, rather these are the most common components:

Volume:

How much the beneficiary is paid in the event of the employees death. There are two different methods for calculating the Group Life volume:

- Flat amount: Everyone in the class receives the same amount of Life benefit, regardless of their salary. There is typically a minimum amount of flat life insurance that the insurer will require, usually around $20k.

- Salary based: A multiple of the employees salary is used to calculate the amount of Life insurance. One or two times salary are the most common multiples. Note that the maximum amount would still apply (see below) so the actual benefit payment may be capped.

Group Life benefits often have a graded schedule, which means the volume is reduced once the employee reaches a certain age. For example, the life benefit may reduce 50% at age 70, or drop to a certain flat amount. There can be more than one reduction, for example, a reduction at age 70 and a further reduction at age 75. Employees typically require less life insurance as they get older, as expenses such as mortgages and children’s education are often paid off at this point. Having a graded schedule also helps to keep the rates down for Group Life. As Life is a pooled benefit the rates are calculated using an age volume distribution, which means having less volume on older employees helps to control the overall rate for that class.

Termination Age:

The age at which the Group Life benefit ceases to be paid. 75 is a common Group Life term age, but there is a great deal of flexibility regarding how high the termination age goes for Group Life, particularly if there is a reduction schedule. Note that the employee still needs to meet the plans eligibility requirements, for example they still have to be working the required number of hours.

Non-Evidence Maximum:

The Non-Evidence Maximum (NEM) is the amount of Group Life coverage a carrier will automatically provide to all employees that are eligible. Any Life coverage in excess of the NEM will typically need to be medically underwritten on an employee by employee basis. Higher NEMs are therefore a benefit to the client as it will reduce medical underwriting. The size of the group and the average Life amount are the two factors typically used by insurers to determine the Life NEM, with larger groups and higher average Life amounts receiving larger NEMs.

The NEM is a major advantage of Group Life insurance over Individual life insurance. Because of the NEM, employees that would be ineligible for Individual life coverage for health reasons can still get Group Life coverage up to the Non-Evidence Maximum.

Maximum:

The maximum amount of Life benefit that will be paid out. This number only affects employees with Life volumes above the maximum. For example, if the Life volume is 2X salary and the maximum is $100k, then someone earning $40k a year won’t be affected by the maximum, but someone earning $55k would be (they would lose $10k of Life benefit).

The maximum is commonly applied to the Basic and Optional Life amounts combined.

Rates:

Rates for Group Life are expressed per $1,000 of volume. For example, if the life rate was $0.20/$1000 and an employee had a flat $50,000 life benefit, then they would pay $10 a month for their life coverage (($50,000/1000) * 0.2 = $10)

While everyone in the same class pays the same rate, the monthly amount they pay will differ if the volume is salary based.

Premiums for Group Life can be covered by either the employee or the employer.

.

Dependant Life:

While technically a separate benefit, the core concept is the same, only reversed. In the event that an employees dependants pass away, a small benefit is paid to the employee. Dependant Life is always a flat benefit, with a common setup being a benefit amount for the spouse or common law partner and half as much for any children that meet the definition of dependant. For example, the spouse may be covered for $10k and the children for $5k each. It is rare to see large Dependant Life volumes, the intention is to provide assistance with costs such as funeral expenses.

.

Optional Life:

Optional Life can be extended to the employees of a Group Life plan. Optional Life is purchased by the employees in addition to the Group Life coverage provided by the plan. Each employee can choose how much (if any) Optional Life to purchase. The key difference is that medical underwriting is usually required for all Optional Life, and Optional Life coverage is always paid for by the employee, not by the employer.

Optional Life may not be the best choice for employees looking to provide adequate life coverage as it is often not portable, meaning if the employee goes to work somewhere else they may not be able to bring their optional life coverage with them.

]]>Notice: compact(): Undefined variable: limits in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

Notice: compact(): Undefined variable: groupby in /hermes/bosnacweb08/bosnacweb08ag/b1302/nf.pillowponcho/public_html/wp-includes/class-wp-comment-query.php on line 853

.

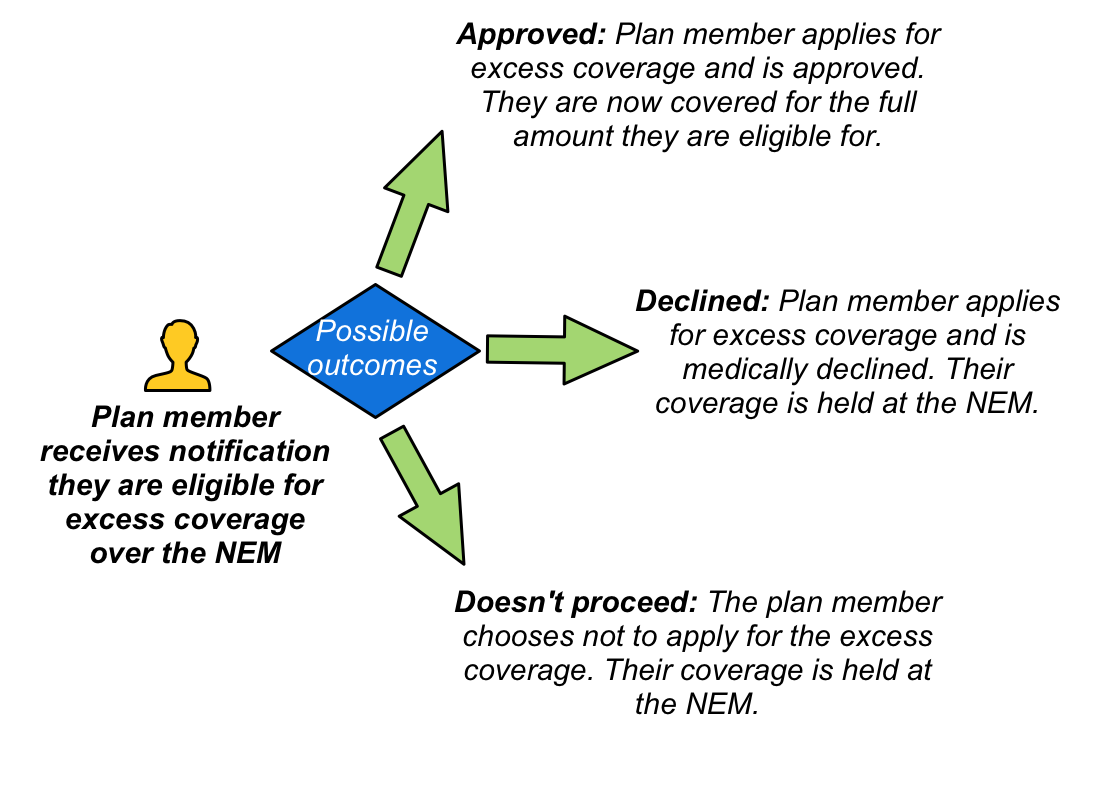

Why am I being medically underwritten?

A common question from employees is why am I being medically underwritten? This can be particularly concerning for employees if some members of the group are being medically underwritten and others aren’t.

There are two main scenarios that would lead to medical underwriting on a Group policy:

- Coverage above the Non-Evidence Maximum: When employees are eligible for coverage above the NEM then medical underwriting is required to approve this addition coverage. Note that even if the employee is declined excess coverage for medical reasons they will still have the coverage up to the NEM. Also note that one benefit may be approved while others are declined. For example, a medical condition may pose an unacceptable disability risk, but not increase the risk of death.

- Late enrolee: If an employee chooses to waive all coverage of the benefits plan but later decides to join the plan then medical underwriting from first dollar may be required. This means if the employee fails the medical underwriting they will not have any coverage, even up to the NEM amount. Note that medical underwriting is typically not required if EHB and Dental were waived due to the employee having coverage through their spouse.

An overview of the three outcomes of Medical Underwriting

Types of medical underwriting

There are different levels of medical underwriting, depending on insurance carrier guidelines and the amount of coverage being requested:

.

Medical Questionnaire

The simplest form of medical underwriting is the completion of a medical questionnaire. Depending on the answers provided in this form, a medical underwriting decision may be able to be made without any further tests.

Sometimes the answers on this initial form will trigger a more detailed questionnaire. For example, if an employee mentions on their medical questionnaire that they recently had knee surgery, then they may be asked to fill in a more detailed questionnaire specific to knee injuries.

It is important to be truthful on the medical questionnaire. The information provided is often validated with the employees doctor to ensure accuracy. In addition, any future claims may be deemed void if it becomes apparent that the medical questionnaire was not completed accurately.

.

Medical exam

A medical exam may be required to complete the medical underwriting process. The usual process is that a registered examiner will contact the employee to arrange a time and place to meet and perform the assessment. This can be at the employees home or at work, or another convenient location that affords suitable privacy.

As part of the examination, the employee will answer a series of questions and their height and weight will be measured. Fluids may also be required as part of this assessment, including urine and blood. More comprehensive tests such as echocardiograms may be required, depending on the coverage being requested.

A final decision can take several days once all the required information has been received.

.

Frequently Asked Questions

Here are some questions that employees may ask, and how to answer them:

- I was recently approved for individual coverage, why was I declined for my group coverage?

For individual coverage, there is an option to ‘rate’ a person depending on the risk they represent. This means older individuals, or those with health conditions, may still be able to get individual coverage, but the rate they pay will be considerably more. For group insurance, rating is not an option. All employees in the same class pay the same rate. The intention of Group medical underwriting is therefore solely to determine if an employee presents a ‘standard risk’. - I was recently medically underwritten somewhere else for group or individual coverage, can they reuse the tests?

This may be an option, depending on which tests were performed and when. Check with your insurance carrier. - My doctor says I am healthy, why am I being declined?

A doctor typically assesses your health at a point in time. The intention of group medical underwriting is to also consider your future risk. Being medically declined for group insurance in no way implies you are not currently healthy. - What if I don’t want the excess coverage over the NEM?

You can choose not to proceed with medical underwriting, but note that you may not have the option to add this additional coverage down the road. You should also ensure that the coverage you have will meet your needs. For example, could you survive for a year if you were unable to work and only receiving 40% of your currently salary? - I’ve been declined. When can I reapply?

This is usually communicated as part of the decline letter. It could be an amount of time, or conditional. For example, you may be eligible to reapply in 12 months, or when you have been symptom free for six months. Some conditions may not allow for reconsideration.